A Beginner’s Guide to Decentralized Finance: What exactly is DeFi?

Preface

You must have heard of the term Decentralized Finance (DeFi) before.

It may have been your colleagues gushing to you about the magic of DeFi, or your cousin bragging to you about his yield farm gains. Whichever it is, this is a term that has dominated 2021 almost as much as NFTs had in 2020.

Said hype notwithstanding, I truly believe that Defi will shape our future in more ways than one. In fact, I truly believe that DeFi is the future.

We are at the precipice of huge change, and DeFi is at the vanguard of it.

But what exactly is DeFi?

In this multi-part series, I will break down DeFi to you, the non-technical reader, in a simple, easy-to-understand, and analogy-driven manner, so that you can — hopefully — be a part of this revolution.

Before I do that however, you must first understand the very thing that the DeFi revolution is looking to disrupt — the traditional global financial system.

Want to read this story later? Save it in Journal.

The traditional global financial system

The 6 components of the traditional global financial system are as follows:

- Money

- Financial Instruments

- Financial Markets

- Financial Institutions

- Regulatory Agencies

- Central Banks

Money

Money constitutes the starting point of the financial system and the means for making an exchange in value. An accumulation of money is a determining factor in defining wealth. Those who store more money are wealthier than those who do not. The consistency of money has a tendency to morph based on changes in the financial system and technology.

Money was once defined by the precious metals silver and gold until it was replaced with the current paper and coin system. As technology constantly evolves, money is now also being defined by electronic transactions. In the recent past, money was accessed by walking into a bank and handing the teller a withdrawal slip. Today, electronic funds are accessed by swiping credit and debit cards and the financial institutions do the rest.

Financial Instruments

Financial instruments are also known as securities, though the layman’s terms are stocks, bonds, mortgages and insurance. At one time, the dealing and trading of stocks was typically exclusive to wealthy individuals who could afford to pay the exorbitant fees charged by stockbrokers.

In recent years, this practice has been made more accessible to the average investor via the introduction of mutual funds that pool the savings of a broad number of investors. By leveraging a high volume of buyers, more investors (and not just wealthy ones) can purchase, trade and accumulate portfolios.

Financial Markets

Financial markets are essentially what you know as trading houses, and these are institutions that are dedicated to the purchase and sale of stocks and bonds. Examples of the more well-known trading houses include the New York Stock Exchange or the NASDAQ.

Buyers and sellers gather at these markets to determine the buying and selling prices for securities, typically with assistance from a stockbroker. Markets will continually fluctuate, resulting in inherent risks with regard to this process.

Financial Institutions

The common term for financial institutions is banks. Though once a brick and mortar building that held money in vaults, modern financial institutions offer a variety of products and services including mortgages, insurance and brokerage accessibility. Financial institutions now compete in the financial market by offering one-stop shopping for financial transactions and advice.

Regulatory Agencies

Regulatory agencies were introduced by the government to provide a check and balance to the activities and influence of financial institutions and markets.

Through thorough examinations and the enforcement of strict guidelines and/or best practices, regulatory agencies closely monitor these big players of the financial system to ensure that the public’s money and investments are in safe and reliable hands.

Central Banks

Almost every country in the world has a central bank that is integral to each country’s government. The founding of central banks was originally a means to finance wars, but today’s central banks manipulate the availability of money and credit in order to control the economy.

They are integral to the stability of the country’s financial system as they oversee national currency and its value. The U.S. Federal Reserve is one of the most important central banks in the modern world, for its actions will indiscriminately affect many other countries around the world.

The problem with the traditional financial system

The global financial system is the foundation that undergirds our societies, allowing for them to even be functional. It represents a pervasive universal system that enables life as we know it, and without which we simply cannot progress, or even — exist.

How else can there be an exchange in value between entities, and how else will people be incentivized to do things in their daily lives that possibly benefit others more than themselves?

The financial system is thus a cornerstone in our lives, and we are heavily dependent on it.

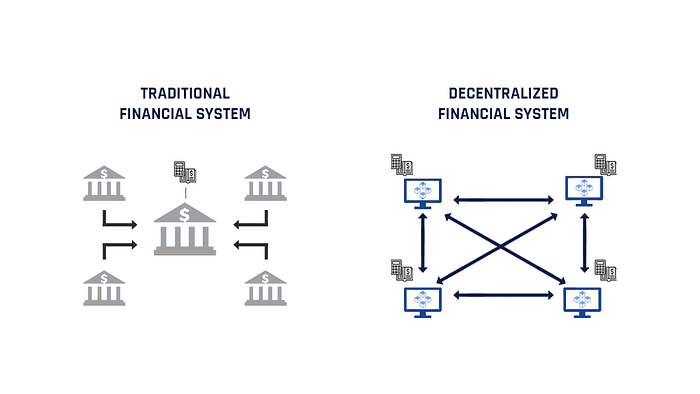

However, since all financial services within the traditional system rely on a central authority of some sort, this centralized ‘hub and spoke’ financial system, or CeFi for short, does have its many risks.

These include mismanagement, fraud and corruption, just to name a few.

Additionally, the financial crisis and, subsequently, the Great Recession, revealed a fatal flaw in this ‘hub and spoke ‘architecture, where the balance sheet problems for a couple of large centralized financial institutions produced a domino effect of tumbling economies and the onset of the global recession.

DeFi as an alternative to the traditional financial system

Across the ages, there have been many brave men and women that have tried to seek an alternative to the CeFi system. Many have failed, but some have succeeded.

Bitcoin, the brainchild of Satoshi Nakamoto is (arguably) one such success story.

Conceived of, and developed as a decentralized currency/money that no one singular entity can control, Bitcoin exists as the epitome of democratization — where power is diffused to the people, not concentrated in the hands of any one institution.

It cannot be controlled by any bank or government, and can be sent to anyone and everyone, by anyone and everyone.

However, transferring money is only the first of many building blocks in a financial system. Aside from sending money to one another, there are a variety of services we use today. For example, loans, saving plans, insurance and stock markets are all services that are built around money, and together, create our financial system.

Although Bitcoin is probably the most well-known blockchain-based alternative to the currency component of the traditional financial system, it is far from the only one in the space.

There are still plenty of other projects helmed by exceptional teams that have attempted, are attempting, and will attempt to radically change the whole DeFi ecosystem, and not just in terms of money and currency.

In fact, as of the time of the writing of this article, there are a whopping 236 extant active DeFi projects in the space.

Collectively, these projects make up the multifaceted DeFi world as we know it.

So, what exactly is DeFi?

In its simplest form, DeFi is a term given to financial services that have no central authority or someone in charge.

Using decentralized money (cryptocurrencies), we can build a multitude of financial services — exchanges, lending services, or insurance companies — that don’t have any owners, and aren’t controlled by anyone.

In other words, DeFi refers to a movement that aims to create an open-source, permissionless, and transparent financial service ecosystem that is available to everyone and operates without any central authority.

You can also think of it as a non-custodial form of finance, where you don’t need to trust a third party like a banker or a bank with your money, in order to do anything with it.

Instead, it uses blockchain technology to disintermediate centralized models, and enables the universal provisioning of financial services for anyone regardless of location, socio-economic class, ethnicity, age, or cultural identity.

This, in my opinion, is the coolest thing about DeFi. Blockchains that support smart contracts enable you to interact with money, and empower you to participate in things like loans, collateralized debt and fundraising, all while being outside of the traditional banking system.

All you ever need is for a way to access the Internet.

How does DeFi work?

To understand how DeFi services are rendered, there is first a need to briefly recap on smart contracts.

If you don’t already have a foundational understanding of what smart contracts are, please go to this article first before moving on.

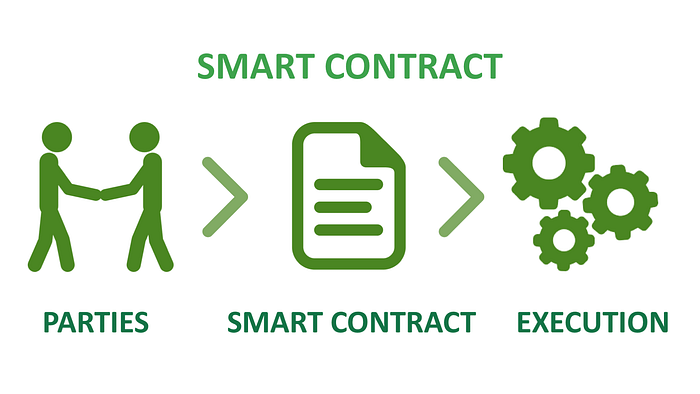

Digital smart contracts enable you to exchange anything of value in a transparent way whilst avoiding the use of a middleman.

So let’s say that Picasso wants to sell an artwork to the Louvre. However, Picasso doesn’t trust that the Louvre will send the money, and the Louvre doesn’t trust that Picasso will actually send them the painting.

This brings up the age-old conundrum of who is supposed to send over their side of the deal first. Alternatively, a middleman could be used to act as an escrow. However, this could be really expensive, and neither Picasso nor the Louvre want to waste needless money on a middleman.

This is where smart contracts could prove useful. The contract could be programmed to only switch the assets if both parties fulfil their side of the bargain: if Picasso sends a digitized artwork deed to the smart contract, and if the Louvre sends 1 billion dollars in Bitcoin to the smart contract.

If both these criteria are fulfilled, the smart contract would automatically execute the trade.

In essence, smart contracts can be programmed to receive and redistribute digital assets. They can also be programmed with custom rule criteria, and transactions made are recorded on a public blockchain. Since records on the blockchain are immutable and fully transparent, the ownership of assets that are transacted via smart contracts also cannot be disputed.

DeFi takes components of traditional finance and decentralizes them by removing middlemen and replacing them with smart contracts. A very straightforward example of this would be decentralized loans.

This way, there is no need for any central authority to manage any given financial transaction or interaction.

What does DeFi allow you to do? (DeFi Services)

Borrowing and Lending

Open lending protocols (or perhaps more commonly known as yield farming protocols) are one of the most popular types of applications that are part of the DeFi ecosystem. Open, decentralized borrowing and lending have many advantages over the traditional credit system. These include instant transaction settlement, the ability to collateralize digital assets, no credit checks, and potential standardization in the future.

Since these lending services are built on public blockchains, they minimize the amount of trust required and have the assurance of cryptographic verification methods. Lending marketplaces on the blockchain reduce counterparty risk, make borrowing and lending cheaper, faster, and available to more people. Interest rates are also usually much lower as compared to those of traditional banks when it comes to borrowing.

Monetary Banking Services

As DeFi applications are, by definition, financial applications, monetary banking services are an obvious use case for them. These can include the issuance of stablecoins, mortgages, and insurance.

For example — because of the large number of stakeholders who need to be involved, the process of getting a mortgage is usually very expensive and time-consuming. With the use of smart contracts however, underwriting and legal fees may be reduced significantly.

Further, a blockchain-based insurance solution could also eliminate the need for intermediaries and allow for a distribution of risk between many participants. This could possibly eventuate in lower premiums (due to middlemen and women being cut out) with the same quality of services.

Decentralized Marketplaces

Arguably, some of the most crucial DeFi applications are decentralized exchanges (DEXes).

These platforms allow for users to trade digital assets without the need for a trusted intermediary (a centralized exchange) to hold their funds for them. Instead, the trades are fully peer-to-peer (P2P), made directly between user wallets with the help of smart contracts.

Because this disintermediation of services will lead to many cost-savings (no middlemen/women fees), decentralized exchanges typically have lower trading fees than centralized exchanges.

Apart from DEXes, blockchain technology may — and have — also be used to issue and allow for the ownership of a wide range of conventional financial instruments, even the more complex ones. These applications would work in a decentralized way that cuts out custodians and eliminates single points of failure.

Security token issuance platforms, for example, provide the tools and resources for issuers to launch tokenized securities on the blockchain with customizable parameters. Many other projects also allow the creation of derivatives, synthetic assets, decentralized prediction markets, and many more.

However, as the evolution of blockchain technology in this particular space is still in its infancy and exploratory stage, there are many risks involved with regard to using these platforms as an end-user.

The current state of DeFi

Now that you know what DeFi is all about, how it works at a generic level, and its potential use-cases — what is the extant state of this ever-changing landscape and ecosystem?

As I had just alluded to, DeFi is still in the beginning stages of its growth and evolution. I strongly believe that the DeFi ecosystem has hardly been definitively shaped in any form and size at all, as that is a process that will likely take another few more years at the very least.

As of March 2021, the total value locked (TVL) in DeFi contracts is more than $41 billion, where TVL is calculated by multiplying the number of tokens in the protocol and their value in USD.

Although the total figure for DeFi may sound substantial, it is important to remember that it is notional because many DeFi tokens lack sufficient liquidity and volume to trade in crypto markets.

Benefits of DeFi

By now, you should also probably be able to envision the advantages that blockchain technology will bring to the finance world.

These include, but are not limited to:

- Security: First, blockchain-based architecture eliminates single points of failure and reduces the need to place data in the hands of intermediaries. This is perfect when it comes to dealing with monetary transactions (as finance platforms do), as the blockchain will ensure that no third-party middlemen will be able to — intentions notwithstanding — mismanage, misappropriate or manipulate the users’ funds in any shape or form, fostering trust in the platforms

- Transparency: Next, blockchain technology allows for the standardization of shared processes, and produces a single shared source of truth for all network participants. Every transaction ever conducted on a blockchain platform will also be immutably recorded onto it, and can be made accessible for anyone to view and audit if required. This has a lot of value when it comes to DEXes, or any finance platform that potentially has to deal with coordination failures in any way, for that matter.

- Programmability: Further, blockchain technology also allows for a reliable automation of business processes through the creation and execution of smart contracts. This can range from simple things like Picasso’s aforementioned deal with the Louvre, to more complex processes like an entire organisation’s workflow management

- Non-custodial: Flowing from the above, third-party custodians are rendered obsolete, as these business processes will no longer require their facilitation. On top of what was already mentioned under the point on security, this can also potentially save a lot of costs for businesses, as well as enable a higher degree of flexibility that would otherwise not be accorded if there existed middlemen and women to appease, navigate around and coordinate with.

- Democratization: Finally, blockchain technology also renders it such that any given platform built on it will be accessible to anyone and everyone regardless of geographical location or jurisdictions. All users need is the ability to connect to the Internet and a smartphone. As both of these are readily available to almost everyone in the world (even those in developing nations), this allows for an effective breaking down of traditional barriers to access in a multitude of ecosystems. Viewed in the context of DeFi, blockchain technology will thus grant previously unbanked individuals a very unique chance to partake in the finance and banking system without even having to set up a traditional bank account.

The challenges that DeFi face

However, and as with all things, DeFi is not perfect; it has its many flaws and downsides too. Further, this is a field that deals with real money, so a lot more is potentially at stake here for end-users who are actively partaking in the ecosystem.

It is therefore of utmost importance that you are aware any way.e of all these said flaws and downsides before you even begin to do so,

Usability

A major issue with the DeFi ecosystem is that it is pretty complicated for your typical person to understand, and to participate in. In order to do so, you’re probably going to need to use digital cryptocurrency wallets like Meta Mask, and that’s undoubtedly not a straightforward task at all, even for the average user.

This may constitute a barrier of entry that will ruthlessly leave out, or even discriminate against, those without the right knowledge and skills to navigate the space.

Oftentimes, and in this case, it is the very people that we want to help (those in developing countries) that sadly will be left out. I mean, if they already have issues opening up a bank account, I definitely do not foresee them being willing or able to use Meta Mask in any way.

Smart Contract vulnerabilities

As aforementioned, smart contracts do allow for a disintermediation of certain processes and services that reduces a system’s dependency on third-party middlemen/women entities, thereby preventing singular points of failure within the system.

However, if not written rigorously, these smart contracts themselves can actually be that singular of failure in and of itself. This is because ultimately, it is still humans who are programming and developing these smart contracts, and as we all should know very well — humans are always prone to errors; that is in our very fallible nature.

Smart contracts have had issues in the past where people didn’t define the rules for certain services correctly, and hackers found creative ways to exploit existing loopholes in order to steal money. The most high-profile example for this would definitely be the DAO hack on Ethereum in 2016.

Another concern is that if not coded and audited properly, smart contracts may have bugs in them that may be potentially fatal to the system that it undergirds. There have been numerous occasions where bugs have occurred and users have lost their funds by having them stuck in the smart contract.

Now, that’s a pretty scary risk that people are taking up by participating in the DeFi ecosystem, and also potentially an extremely devastating one for those in developing countries who may have their very livelihoods and survivability at stake here.

However, the good news is that there are now several decentralized insurance projects like Nexus and CDX that can help hedge said risks for users, so you would do well to look into them before dipping your toes into the DeFi world!

That said, if you do eventually decide to test out any of the DeFi services that are available in today’s market, it is still always best to only do so with an amount of money that you can afford (and are willing) to lose, in case anything goes wrong.

Scams

In a similar vein — because of how new and relatively unexplored this DeFi space really is, many different vectors of attack are likely still left open for potential hackers to exploit.

As a result, scams are still pretty abundant in this space. DeFi “rug pulls,” in which hackers drain a protocol of funds leaving investors unable to trade or liquidate their assets, are extremely common, even on established platforms like Polygon or Binance Smart Chain.

Regulatory and liability concerns

The open and relatively distributed nature of the decentralized finance ecosystem might also pose problems to existing financial regulation. Current laws were crafted based on the idea of separate financial jurisdictions, each with its own set of laws and rules. DeFi’s borderless transaction span presents important questions for this type of regulation. For example, who is culpable in a financial crime that occurs across borders, protocols, and DeFi apps?

Smart contracts are another area of concern for DeFi regulation. Aside from Bitcoin’s success, DeFi is the clearest example of the “code is law” thesis, wherein law represents a set of rules that are written and enforced through immutable code. The smart contract’s algorithm is encoded with the necessary constructs and terms of use to conduct transactions between two parties. However, software systems can malfunction due to a wide variety of factors.

For example, what if an incorrect input causes a system to crash? Or, if a compiler (which is responsible for compiling and running code) errs. Who is liable for these changes? These and many other questions need to be worked out before DeFi becomes a mainstream system used by the masses.

Fiat-Crypto value transfer friction

Finally, another major stumbling block to democratizing access to financial services is actually the friction and inertia to transfer value into and out of the crypto-verse.

To put it into perspective, it may be very difficult for a non-banked person to trade their local currency for cryptocurrencies in order to participate in the DeFi ecosystem. All extant methods currently require at least a little bit of technical knowledge to utilise, and this may be something that many unbanked individuals may not have the luxury of exposure to.

Closing (Personal) Thoughts on the DeFi ecosystem

I sincerely hope that this article has at least helped you to better understand what DeFi really is — a term given for a variety of decentralized financial services that aim to replace our current centralized financial system.

This is a fantastic time for you to think about DeFi as a concept at a deeper level, for it seems that the DeFi revolution has only just reached its early adopter stage, and the coming years will be very telling with regard to its capacity to cross the chasm into mainstream adoption.

If DeFi represents an epochal wind of change, it would do you quite a bit of good to stand at the vanguard of that.

There’s no doubt that a decentralized financial system can benefit many different segments of the global population that currently suffer from financial discrimination, high fees and inefficiencies in managing their funds.

For me, I sincerely hope that this is where the DeFi ecosystem is headed towards.

To put it into perspective: according to the World Bank, an incredible 1.7 billion adults in the world don’t have access to a bank account. In other words, the world banks have excluded 1.7 billion adults from access to basic financial services like loans, mortgages and even insurance.

WIth DeFi loans, a bank account would no longer be needed; the greedy banker would be cut out, and the world’s unbanked population would be able to get access to these financial services with just a few taps of their smartphone.

I’m also extremely fascinated by the potential role that DeFi could play in developing nations. When I look around the world, there are plenty of countries in South America that are experiencing rampant inflation.

Venezuela is at the forefront of everyone’s mind here, and you can see why that is the case when it takes this much money to buy a roll of toilet paper.

In essence, it’s cheaper to wipe your behind in Venezuela with fiat money, than with toilet paper! This is a pretty mind-blowing fact, but a very uncomfortable one too at that.

People in developing countries with high inflation like Venezuela or Argentina thus severely need access to a stable asset to preserve their purchasing power.

This is exactly what DeFi can accord them.

For example, a project like Compound Finance will allow for people from these countries to swap out their local currency for the DAI stablecoin. This will ensure that the value these people hold will not fluctuate and disappear with the local currency itself.

Moreover, they will also be able to lend out their DAI coins on the Compound platform if they want to, in order to earn interest on the value of their holdings.

This is why I’m really excited about DeFi in this particular context, for it readily offers these people the tools to protect themselves and their families against rapidly inflating local currency, whilst also giving them many good opportunities to grow their wealth — all outside of the traditional banking system that many of them have no access to anyway.

Right now, I feel like the DeFi ecosystem is too unfairly skewed in favor of the more privileged and the ‘haves’ — only those with ample resources (to lose) are able to truly benefit from the extant DeFi ecosystem.

I mean, can you really see a crop farmer from Venezuela putting his hard-earned sweat money into a yield farm or vault? They simply have too much to lose, and are unable to leverage on these DeFi protocols to grow their capital.

I really hope to see more DeFi projects that are more geared toward these groups of people, and whose goals are to truly serve the underserved. They may not have monetary resources to provide, but they definitely do possess other talents and skills that can be tapped on. Projects like Axie Infinity are a great start with regard to that.

For me, the success of DeFi really rides on this — we as a global community are only as strong and great as our weakest link.

If you found this article useful, do give my account a follow — there will be many more such DeFi articles to come!

Enjoyed this post? Subscribe to the Machine Learnings newsletter for an easy understanding of AI advances shaping our world.